Delivra Health Brands Inc.

FY2025 Beat: Geographic Expansion and Potential M&A in the Works

Published: Oct 9, 2025

Author: FRC Analysts

*Delivra Health Brands Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

Sector: Healthcare | Industry: Drug Manufacturers-Specialty & Generic

Ticker Symbols: DHBUF – NASDAQ DHB.V – TSX

Report Highlights

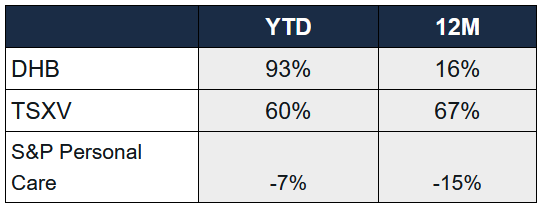

- DHB’s share price is up 93% YTD, outperforming the S&P Personal Care Index, which fell 7%.

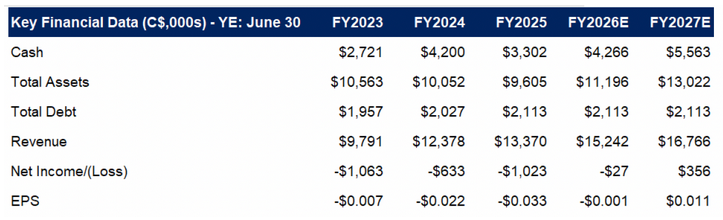

- FY2025 (ended June 30, 2025) revenue grew 8% YoY, beating our estimate by 3%, driven by stronger-than-expected Dream Water sales in the U.S. and Middle East.

- Marketing costs rose 26% YoY to 15% of revenue, reflecting management’s earlier guidance to increase marketing spend to drive growth. Adjusted EPS fell 12% to ($0.02), beating our estimate of ($0.04) due to higher revenue and lower costs.

- DHB sells sleep aid products under the Dream Water brand, and pain relief products under LivRelief and LivRelief Infused brands. Approximately 80% of FY2025 sales came from the U.S. and Middle East (up from 74% in FY2024), with the remaining 20% from Canada. Products are available at over 30k+ distribution points, including retail and pharmacy chains, convenience stores, and airports. DHB is actively expanding distribution in the Middle East, and Latin America to support long-term growth.

- We note that market sentiment for the Personal Care sector is down slightly, with a 3% drop in average sector forward EV/revenue since May 2025. However, the sector is expected to accelerate, with consensus revenue growth rising to 11% in 2025, from 9% in 2024.

- DHB maintains a healthy balance sheet, and is well funded to support its expansion plans. We anticipate robust organic growth, supported by growing awareness of the importance of sleep for mental and physical health, alongside additional expansion through new geographic markets.

- The company is also planning M&A to expand its product portfolio — a strategy we view positively. With robust distribution channels, we believe DHB can quickly increase shelf space for acquired products, boost revenue, and deliver accretive value.

- We’re excited to launch our new video series — Stocks in Real Life — connecting the world of capital markets to relatable, real-world stories and concepts. Check out our first episode, featuring Delivra: https://www.youtube.com/shorts/_yxQOhv_C50

Fundamental Research Corp. Equity Rating Scale:

Fundamental Research Corp. Equity Rating Scale (ratings are not a recommendation to acquire, dispose of, or take no action regarding a security; the definition of our ratings are explained below):

- Buy – Fair value is 12% above the current market price; or risk and reward is favorable

- Hold – Fair value is between 5% to 12% above the current market price

- Sell – Fair value is 5% above, or less, than the current market value; or risk and reward is unfavorable

- Suspended or Rating N/A – Coverage and ratings suspended until more information can be obtained from the company regarding recent events.

Fundamental Research Corp. – Risk Rating Scale:

- (Low Risk) – The company operates in an industry where it has a strong position (for example a monopoly, high market share etc.) or operates in a regulated industry. The future outlook is stable or positive for the industry. The company generates positive free cash flow and has a history of profitability. The capital structure is conservative with little or no debt.

- (Below Average Risk) – The company operates in an industry where the fundamentals and outlook are positive. The industry and company are relatively less sensitive to systematic risk than companies with a Risk Rating of 3. The company has a history of profitability and has demonstrated its ability to generate positive free cash flows (though current free cash flow may be negative due to capital investment). The company’s capital structure is conservative with little to modest use of debt.

- (Average Risk) – The company operates in an industry that has average sensitivity to systematic risk. The industry may be cyclical. Profits and cash flow are sensitive to economic factors although the company has demonstrated its ability to generate positive earnings and cash flow. Debt use is in line with industry averages, and coverage ratios are sufficient.

- (Speculative) – The company has little or no history of generating earnings or cash flow. Debt use is higher. These companies may be in start-up mode or in a turnaround situation. These companies should be considered speculative.

- (Highly Speculative) – The company has no history of generating earnings or cash flow. They may operate in a new industry with new, and unproven products. Products may be at the development stage, testing, or seeking regulatory approval. These companies may run into liquidity issues and may rely on external funding. These stocks are considered highly speculative.

Definition of FRC’s Fair Value Estimate – Our fair value estimate is the theoretical value of the company’s equity using widely accepted methods of valuation such as discount cash flow or comparables. IT IS NOT A TARGET PRICE or PREDICTION OF THE FUTURE STOCK PRICE.

Disclaimers and Disclosure

Analyst Certification: The views expressed in this report accurately reflect the personal views of the analyst, and no part of their compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed.

Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The analyst and Fundamental Research Corp.

Fundamental Research Corp. “FRC” owns shares of the subject company: No. The analyst owns shares of the subject company: No , does not make a market or offer shares for sale of the subject company, and does not have any investment banking business with the subject company.

Annual fees ranging from $15,000 to $30,000 have been paid to FRC by Yorkton Equity Group Inc. to commission this report and research coverage including update reports. This fee creates a potential conflict of interest which readers should consider. FRC takes steps to mitigate conflicts including setting fees in advance and utilizing analysts who must abide by CFA Institute Code of Ethics and Standards of Professional Conduct. Additionally, analysts may not trade in any security under coverage. Our full editorial control of all research, timing of release of the reports, and release of liability for negative reports are protected contractually. The issuer has agreed to a minimum of three updates and coverage cannot be unilaterally terminated. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time.

The distribution of FRC’s ratings are as follows: BUY (69%), HOLD (3%), SELL / SUSPEND (28%). Yorkton Equity Group Inc.

This report contains “forward looking” statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company’s products/services in the marketplace; acceptance in the marketplace of the Company’s new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company’s periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward-looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. A report initiating coverage will most often be updated quarterly while a report issuing a rating may have no further or less frequent updates because the subject company is likely to be in earlier stages where nothing material may occur quarter to quarter.

Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report.

The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.