Tungsten market fundamentals have strengthened materially, supported by higher benchmark APT prices that have recently moved above US$1,000/MTU amid robust defence-driven demand and a tightening supply environment. China’s export controls implemented in 2025 have reinforced structural supply constraints and accelerated Western efforts to diversify sourcing. Against this backdrop, we adopt a higher long-term price framework, increasing our APT assumption to US$800/MTU from US$450/MTU previously.

Operationally, Almonty has transitioned into its next growth phase with the Sangdong Tungsten Mine entering active operations in December 2025 and commencing a staged ramp-up toward nameplate capacity by 2027. Beyond Sangdong, the company is advancing multiple levers for medium-term growth, including capacity expansion at Panasqueira, reserve definition at the Sangdong Molybdenum project, and development progress at Gentung Browns Lake toward potential production readiness in 2H26. Reflecting improved pricing assumptions and clearer production visibility, we update our fair value estimate to C$19.30 per share (from C$7.69 previously) and maintain a HOLD rating.

Investment Highlights

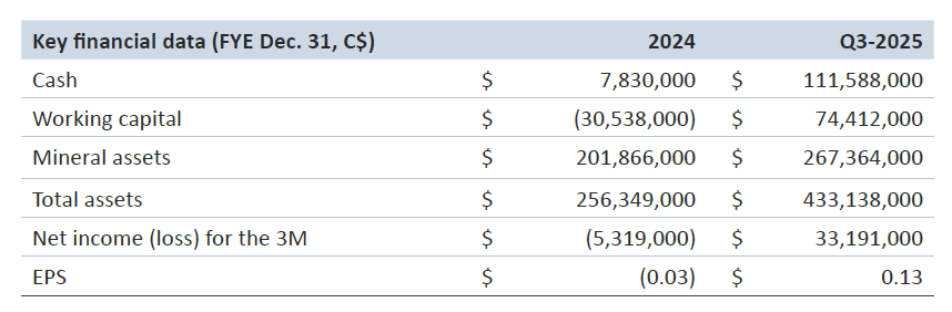

- Almonty Industries Inc. (TSX: AII, ASX: AII, OTC: ALMTF, FRA: ALI) (“Almonty” or the “Company”) is a multi-asset owner that develops and operates tungsten projects. Its assets include development projects and a producing mine. The Company’s share price has increased approximately 25x (2,445%) since our initial coverage report in February 2023.

- Higher tungsten prices: Benchmark APT prices have recently moved above US$1,000/MTU, with spot levels cited around US$1,125 to US$1,150/MTU, driven by strong demand from defence-related end markets and a tighter supply environment. China, which controls more than 80% of global tungsten supply, has imposed export controls in 2025, reinforcing supply constraints and accelerating efforts by Western economies to diversify sourcing away from Chinese production. These market dynamics support a structurally higher tungsten price deck in our model. As such, we increase our APT price assumption to US$800/MTU versus the prior estimate of US$450/MTU.

- Ramp-up at Sangdong: The Sangdong Tungsten Mine entered active operations in December 2025 with the delivery of the first ore, marking the transition from construction to production and the start of ramp-up. The ramp-up is structured in two phases, with Phase 1 targeting a production rate of 640,000 tpa by mid- 2026, followed by Phase 2, which is expected to double capacity to approximately 1.2 million tpa by 2027.

- We update our fair value estimate to C$19.30 per share (earlier C$7.69) and maintain our HOLD rating.

Significant growth potential at other projects: Beyond Sangdong, Almonty Industries is advancing multiple growth initiatives. Drilling at Panasqueira supports expansion into a new Level 4, targeting potential output of up to ~124,000 MTUs and extended mine life. Sangdong Molybdenum (0.26% MoS₂) is progressing toward reserve definition, while Gentung Browns Lake is being advanced toward production readiness by 2H26, with potential output of ~140,000 MTUs.

This report has been prepared by an analyst on contract with or employed by Couloir Capital Ltd. The analyst certifies that the views expressed in this report, which include the rating assigned to the issuer’s shares as well as the analytical substance and tone of the report, accurately reflect his or her personal views about the subject securities and the issuer. No part of his / her compensation was, is, or will be directly or indirectly related to the specific recommendations.

Couloir Capital, its affiliates, and their respective officers, directors, representatives, researchers, and members of their families may hold positions in the companies mentioned in this document and may buy and/or sell their securities. Additionally, Couloir Capital may have provided, in the past and may provide, in the future, certain advisory or corporate finance services and receive financial and other incentives from issuers as consideration for the provision of such services.

Couloir Capital has prepared this document for general information purposes only. This document should not be considered a solicitation to purchase or sell securities or a recommendation to buy or sell securities. The information provided has been derived from sources believed to be accurate, but cannot be guaranteed. This document does not consider the particular investment objectives, financial situations, or needs of individual recipients and other issues (e.g., prohibitions to investments due to law, jurisdiction issues, etc.) that may exist for certain persons. Recipients should rely on their own investigations and take their own professional advice before making an investment. Couloir Capital will not treat recipients of this document as clients by virtue of having viewed this document.

Company-specific disclosures, if any, are below:

1. In the last 24 months, Couloir Capital Ltd. has been retained by the subject issuer under a service agreement that includes analyst research coverage.

2. The views of the Analyst are personal.

3. No part of the Analyst’s compensation was directly or indirectly related to the specific ratings as used by the research Analyst in the Reports.

4. The Analyst does not maintain a financial interest in the securities or options of the Company.

5. The principal of Couloir Capital maintains a financial interest in the securities or options of the Company through an affiliated hedge fund entity.

6. The information contained in the Reports is based upon publicly available information that the Analyst believes to be correct but has not independently verified with respect to truth or correctness.

Investment Ratings -Recommendations

Each company within an analyst’s universe, or group of companies covered, is assigned:

1. A recommendation or rating, usually BUY, HOLD, or SELL;

2. A 12-month target price, which represents an analyst’s current assessment of a company’s

potential stock price over the next year; and

3. An overall risk rating which represents an analyst’s assessment of the company’s overall investment risk.

These ratings are more fully explained below. Before acting on a recommendation, we caution you to confer with your investment advisor to determine the suitability of our recommendation for your specific investment objectives, risk tolerance, and investment time horizon.

Couloir Capital’s recommendation categories include the following:

Buy

The analyst believes that the security will outperform other companies in their sector on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) BUY rating.

Hold

The analyst believes that the security is expected to perform in line with other companies in their sector on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) HOLD rating.

Sell

Investors are advised to sell the security or hold alternative securities within the sector. Stocks in this category are expected to under-perform other companies on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) SELL rating.

Tender

The analyst is recommending that investors tender to a specific offering for the company’s stock.

Research Comment

An analyst comment about an issuer event that does not include a rating.

Coverage Dropped

Couloir Capital will no longer cover the issuer. Couloir Capital will provide notice to clients whenever coverage of an issuer is discontinued. Following termination of coverage, we recommend clients seek advice from their respective Investment Advisor.

Under Review

Placing a stock Under Review does not revise the current rating or recommendation of the analyst. A stock will be placed Under Review when the relevant company has a significant material event with further information pending or to be announced. An analyst will place a stock Under Review while he/she awaits enough information to re-evaluate the company’s financial situation.

The above ratings are determined by the analyst at the time of publication. On occasion, total returns

may fall outside of the ranges due to market price movements and/or short-term volatility.

Overall Risk Rating

Very High Risk: Venture-type companies or more established micro, small, mid or large-cap companies whose risk profile parameters and/or lack of liquidity warrant such a designation. These companies are only appropriate for investors who have a very high tolerance for risk and volatility and who can incur a temporary or permanent loss of a very significant portion of their investment capital.

High Risk: Typically, micro or small-cap companies which have an above-average investment risk relative to more established or mid to large-cap companies. These companies will generally not form part of the broad senior stock market indices and often will have less liquidity than more established mid and large-cap companies. These companies are only appropriate for investors who have a high tolerance for risk and volatility and who can incur a temporary or permanent loss of a significant portion of their investment capital.

Medium-High Risk: Typically, mid to large-cap companies have a medium to high investment risk. These companies will often form part of the broader senior stock market indices or sector-specific indices. These companies are only appropriate for investors who have a medium to high tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital

Moderate Risk: Large to very large cap companies with established earnings who have a track record of lower volatility when compared against the broad senior stock market indices. These companies are only appropriate for investors who have a medium tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital.