PEA delivery (Q2/2026). We model Converse at ~155 Koz/year gold production at an AISC of US$1,902/oz and a 16-year life of mine. We believe that there is further potential for mine plan optimization and gold recovery assumptions to push the production profile at a higher rate at a lower AISC.

Financing close (expected in February 2026). Confirmation of $32.64M close and early capital deployment into drilling, metallurgy, and permitting work streams.

Drill results (Q1/Q2 2026) from the planned ~30,000 m drill program for 2026.

PFS technical studies. Updates from technical work done to support the PFS, including updates on environmental baseline study work and additional metallurgical testwork.

Valuation and recommendation Our price target of $6.75/share, which implies a ~200% upside to RM’s latest close, is based on a 0.5x blended NAV multiple at US$3,500/oz LT gold price assumption. Our conceptual DCF values Converse at $1,031M (NPV5%), yielding a total company NAV of ~$1,150M or ~C$13.50/share fully diluted and fully funded to feasibility study & construction readiness. Non-core assets (Rattlesnake Hills, Wyoming; Newton, BC) are assigned a combined $38.6M in-situ value. We assume a $50M equity raise in 2027 at $4.00/share, strategically timed to follow key de-risking milestones. We maintain our Buy rating for the stock.

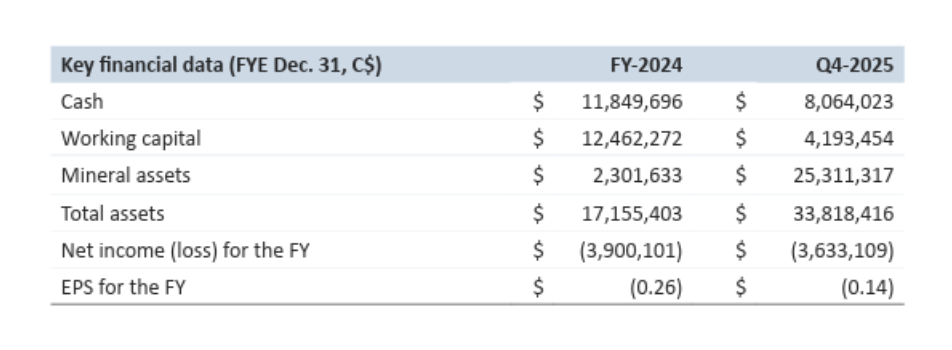

Since our initiation on Axcap Ventures (now Roxmore Resources, TSXV: RM, OTC: GARLF, FF: 1WJO), in August 2025, the company has undergone a comprehensive corporate transformation. The transformation started with the acquisition of Taura Gold (closed on November 20, 2025), which essentially brought in a new management team with a solid track record of project execution and multi-billion dollar exits in Nevada (Fronteer Gold) and West Africa (Roxgold). The transaction was concurrent with a 10:1 share consolidation, a $9.16M strategic financing, and a corporate rebrand to Roxmore Resources. Subsequently, Roxmore has continued focusing on resource upgrade & extension drilling, commissioned a PEA (expected in Q2/2026), uplisted to TSX, and announced a $30M non-brokered private placement (increased to $32.64M), with focus on de-risking the Converse Gold Project. Our investment thesis remains largely unchanged and is anchored around the Converse Gold Project.

With a total resource base of ~5.9 Moz grading at 0.52 g/t Au (5.57 Moz at 0.52 g/t Au M&I and 0.42 Moz at 0.53 g/t Au Inferred), Converse is one of the largest undeveloped gold deposits i n Nevada, which is not owned by a major gold producer. With this update, we have also updated our model and our price target to $6.75/share. The revision is largely driven by the gold price assumption of US$3,500/oz from US$2,700/ oz as well as 10:1 share consolidation which has led to the change in price target on a per share basis. On an EV/oz basis, the stock trades at US$14/oz, a deep discount compared to peers at US$105/oz. We view the valuation gap to close as the new management continues to work towards de-risking Converse on all fronts, i.e. technical and environmental permitting. Overall, Roxmore provides a very attractive entry point into a potential low-risk, low-complexity project in a Tier 1 mining jurisdiction.

This report has been prepared by an analyst on contract with or employed by Couloir Capital Ltd. The analyst certifies that the views expressed in this report, which include the rating assigned to the issuer’s shares as well as the analytical substance and tone of the report, accurately reflect his or her personal views about the subject securities and the issuer. No part of his / her compensation was, is, or will be directly or indirectly related to the specific recommendations.

Couloir Capital, its affiliates, and their respective officers, directors, representatives, researchers, and members of their families may hold positions in the companies mentioned in this document and may buy and/or sell their securities. Additionally, Couloir Capital may have provided, in the past and may provide, in the future, certain advisory or corporate finance services and receive financial and other incentives from issuers as consideration for the provision of such services.

Couloir Capital has prepared this document for general information purposes only. This document should not be considered a solicitation to purchase or sell securities or a recommendation to buy or sell securities. The information provided has been derived from sources believed to be accurate, but cannot be guaranteed. This document does not consider the particular investment objectives, financial situations, or needs of individual recipients and other issues (e.g., prohibitions to investments due to law, jurisdiction issues, etc.) that may exist for certain persons. Recipients should rely on their own investigations and take their own professional advice before making an investment. Couloir Capital will not treat recipients of this document as clients by virtue of having viewed this document.

Company-specific disclosures, if any, are below:

1. In the last 24 months, Couloir Capital Ltd. has been retained by the subject issuer under a service agreement that includes analyst research coverage.

2. The views of the Analyst are personal.

3. No part of the Analyst’s compensation was directly or indirectly related to the specific ratings as used by the research Analyst in the Reports.

4. The Analyst does not maintain a financial interest in the securities or options of the Company.

5. The principal of Couloir Capital maintains a financial interest in the securities or options of the Company through an affiliated hedge fund entity.

6. The information contained in the Reports is based upon publicly available information that the Analyst believes to be correct but has not independently verified with respect to truth or correctness.

Investment Ratings -Recommendations

Each company within an analyst’s universe, or group of companies covered, is assigned:

1. A recommendation or rating, usually BUY, HOLD, or SELL;

2. A 12-month target price, which represents an analyst’s current assessment of a company’s

potential stock price over the next year; and

3. An overall risk rating which represents an analyst’s assessment of the company’s overall investment risk.

These ratings are more fully explained below. Before acting on a recommendation, we caution you to confer with your investment advisor to determine the suitability of our recommendation for your specific investment objectives, risk tolerance, and investment time horizon.

Couloir Capital’s recommendation categories include the following:

Buy

The analyst believes that the security will outperform other companies in their sector on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) BUY rating.

Hold

The analyst believes that the security is expected to perform in line with other companies in their sector on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) HOLD rating.

Sell

Investors are advised to sell the security or hold alternative securities within the sector. Stocks in this category are expected to under-perform other companies on a risk-adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) SELL rating.

Tender

The analyst is recommending that investors tender to a specific offering for the company’s stock.

Research Comment

An analyst comment about an issuer event that does not include a rating.

Coverage Dropped

Couloir Capital will no longer cover the issuer. Couloir Capital will provide notice to clients whenever coverage of an issuer is discontinued. Following termination of coverage, we recommend clients seek advice from their respective Investment Advisor.

Under Review

Placing a stock Under Review does not revise the current rating or recommendation of the analyst. A stock will be placed Under Review when the relevant company has a significant material event with further information pending or to be announced. An analyst will place a stock Under Review while he/she awaits enough information to re-evaluate the company’s financial situation.

The above ratings are determined by the analyst at the time of publication. On occasion, total returns

may fall outside of the ranges due to market price movements and/or short-term volatility.

Overall Risk Rating

Very High Risk: Venture-type companies or more established micro, small, mid or large-cap companies whose risk profile parameters and/or lack of liquidity warrant such a designation. These companies are only appropriate for investors who have a very high tolerance for risk and volatility and who can incur a temporary or permanent loss of a very significant portion of their investment capital.

High Risk: Typically, micro or small-cap companies which have an above-average investment risk relative to more established or mid to large-cap companies. These companies will generally not form part of the broad senior stock market indices and often will have less liquidity than more established mid and large-cap companies. These companies are only appropriate for investors who have a high tolerance for risk and volatility and who can incur a temporary or permanent loss of a significant portion of their investment capital.

Medium-High Risk: Typically, mid to large-cap companies have a medium to high investment risk. These companies will often form part of the broader senior stock market indices or sector-specific indices. These companies are only appropriate for investors who have a medium to high tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital

Moderate Risk: Large to very large cap companies with established earnings who have a track record of lower volatility when compared against the broad senior stock market indices. These companies are only appropriate for investors who have a medium tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital.