Doubleview Gold Corp.

Reports $7B Project Valuation; Stock Trades at Just 7% of NPV

Published: Mar 31, 2026

Author: FRC Analysts

Disclosure: Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

Company Details

Sector – Basic Materials

Industry – Other Industrial Metals & Mining

Trading Information

Trading information – DBG.V : TSXV

Report Highlights

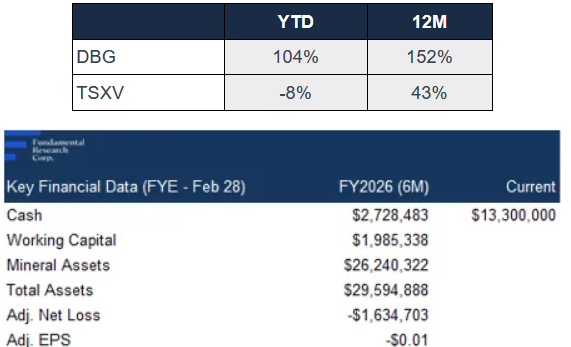

- Outstanding Stock Performance: DBG has been one of the best-performing stocks in our coverage universe. Since we initiated coverage in August 2020, shares are up 637%, and MCAP has risen from $32M to $462M, a 1,347% increase.

- Preliminary Economic Assessment (PEA): An independent economic study on the Hat polymetallic project in the Golden Triangle in B.C shows a large-scale open-pit operation, with a 25-year mine life, AT-NPV5% of $7B, and IRR of 19%, using consensus metal prices. DBG is trading at just 7% of NPV, indicating significant undervaluation. Using February 2026 spot prices, AT-NPV5% rises to $14B, with an IRR of 39%, well above the 15% threshold we consider attractive for mining projects. Initial CAPEX is $3.6B, which is high, but typical for large projects, while cash costs remain at the low end of the industry range, due to significant by-product credits.

- Resource Growth: The latest resource estimate incorporates drilling since 2024, with M&I resources (higher confidence category) up 330% to 6 Blbs CuEq (copper equivalent), and inferred resources up 26% to 5 Blbs. M&I now accounts for 56% of total resources vs 27% previously, reflecting higher confidence. In addition, weighted average grades increased 17%, supporting potential higher production at lower costs. Based on spot prices, gold accounts for 44% of resources, copper 38%, scandium 11%, cobalt 6%, and silver 1%.

- Scandium & Cobalt: Maiden scandium resource added; The rare presence of scandium and cobalt in a copper-gold-rich deposit enhances project attractiveness. Scandium is a critical mineral, used in super-alloys, and ceramic fuel cells. The U.S. imports all of its scandium, underscoring the need for domestic production in North America.

- Metal Price Outlook: Although gold and copper have pulled back from their historic highs, they are up 46% YoY and 4% YoY, respectively. We maintain a positive outlook on gold, supported by safe-haven demand amid geopolitical uncertainty, and projected inflation-driven US$ weakness. Copper also has a positive outlook, supported by US$ weakness, slow production growth, and recent supply disruptions. The market is expected to shift from a surplus in 2025 to a deficit in 2026.

- Next Steps: Resource upgrade and expansion drilling, metallurgical (recovery) tests, and project optimization.

Price and Volume (1-year)

*QP: Erik Ostensoe, P.Geo., Consulting Geologist of Doubleview Gold Corp. Doubleview Gold Corp. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

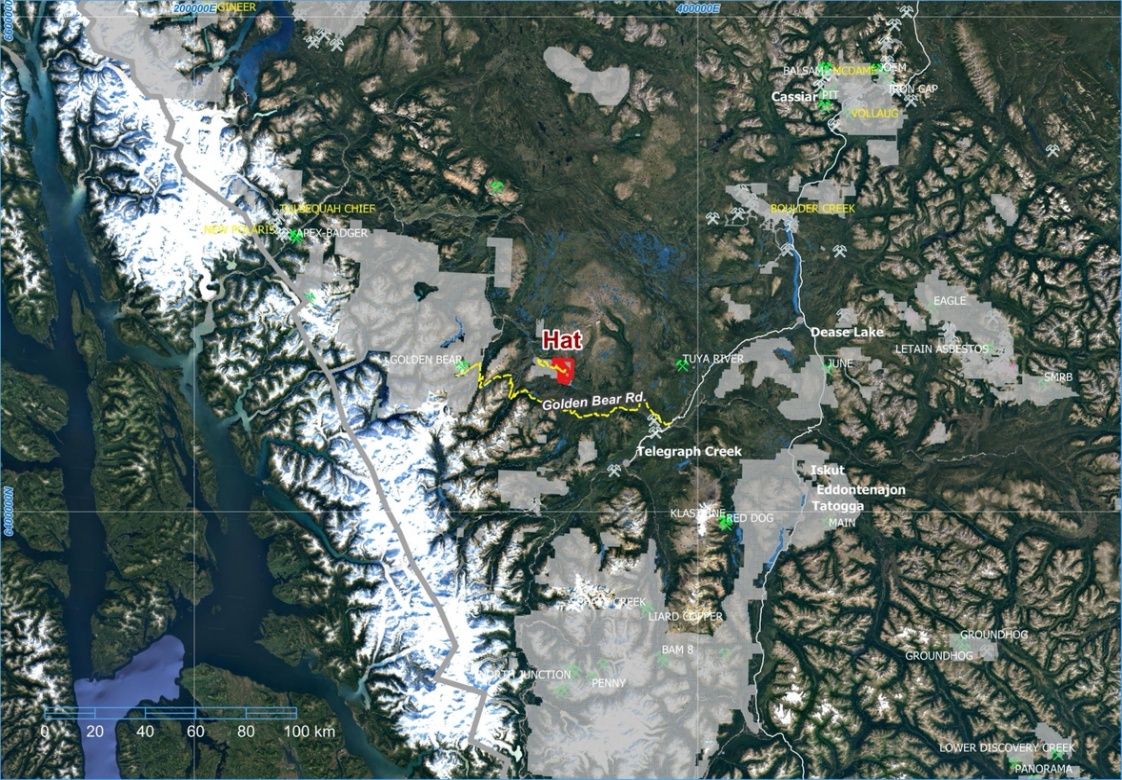

The Hat projected, located in B.C.’s Golden Triangle, one of the world’s most mineralized regions, hosts polymetallic porphyry mineralization containing copper, gold, silver, cobalt, and scandium

Hat Polymetallic Project, B.C. (100% interest)

Project Location

Strategically situated near renowned production and development projects such as Red Chris, Galore Creek, and Schaft Creek

Located in northwestern B.C., 95 km southwest of Dease Lake, and 190 km south of Atlin, the project benefits from access to power, water, and a skilled local workforce

Although the property is remote, future road access may be supported through restoration of a historic access route should the project advance to production. Regional infrastructure prospects strengthened in 2024, when the B.C. government, and the Tahltan Central Government announced a joint $195 M investment to upgrade regional highway infrastructure.

Updated Resource Estimate

The latest resource estimate incorporates drilling completed since the 2024 estimate , and is based on 97 drill holes totaling 49,548 m, up from 71 holes totaling 30,000 m in the prior estimate.

M&I resources (higher-confidence category) increased 330% to 6 Blbs CuEq

To view the complete report, click on the button above.

The opinions expressed in this report are the true opinions of the analyst(s) about any companies and industries mentioned. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The companies listed above are covered by FRC under an issuer-paid model, where fees have been paid to FRC to commission this report and research coverage. This creates a potential conflict of interest which readers should consider. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. To subscribe for real-time access to research, visit https://www.researchfrc.com/plans for subscription options. This report contains “forward looking” statements. Forward-looking statements regarding the Company, industry, and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company’s products/services in the marketplace; acceptance in the marketplace of the Company’s new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company’s periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward-looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.