“War Shocks, Cash Crunch, Market Breakdown: Sector Holds Steady”

The U.S. financial story of early 2026 reads like two different years packed into three months. January and February felt routine, steady growth, stable rates, and calm markets. Then came March: conflict in the Middle East, oil surging past $90 a barrel, and the S&P 500 breaking a trend line that had held since 2025. Investors scrambled, private cash funds froze, and commodity headlines dominated screens. Yet through it all, the sector remained mostly resilient while major indexes dropped nearly 5%.

January–February: The Calm Before the Storm

The first weeks of 2026 looked like a victory lap for the Federal Reserve. Inflation cooled toward 2.6%, and rates stayed at 4.75%. Job markets stayed firm, and credit demand remained moderate.

That changed in late February when war between the U.S. and Iran jolted global markets. Oil prices spiked. Gasoline costs jumped at the pump. Traders instantly priced in “sticky inflation” fears, assuming the Fed would push rate cuts further into the future. Over four weeks, the S&P 500 slid 4–5%, and the Dow saw breathtaking daily swings, down 800 points one day, up 600 the next.

A Technical Warning

For market watchers, the pivotal moment came when the S&P 500 dropped below its 200-day moving average, the market’s unofficial “health line.” Historically, that break has preceded every major recession since the 1980s. Markets flashed red, but core institutions looked like the calmest part of the storm.

Private Cash Funds Hit a Wall

Private equity entered 2026 flush with roughly $1.1 trillion in unspent capital. But fundraising momentum suddenly broke down. Many institutional investors, pensions and endowments, were still waiting for distributions from older deals that hadn’t yet sold. More than half said they had no liquidity to commit to new funds.

The geopolitical shock amplified the strain. Energy and tech deals froze, except for defense related investments. With exits stalled and buyers scarce, private capital’s credit links became a new worry spot.

Banks’ Financial Strength

The latest earnings season confirmed resilience across the sector. Large groups forecast 5–7% growth for 2026, respectable considering war-driven volatility.

Key numbers underscore strength:

- Capital reserves – 13.5%, well above the 10.5% regulatory minimum

- Cash buffers – five-year highs

- Deposits – $3.2 trillion, stable quarter-to-quarter

Stress test simulations show profits strengthening if rates tick up another 2%.

Valuation Gap

Compared to the lofty valuations elsewhere, financial stocks now look cheap. Investors now pay under a dollar for each $1 of book value while paying $4.20 for a similar slice of the broader market, a spread not seen since 2011.

Technology Quietly Changes the Game

While headlines shouted “war” and “sell-off,” modernization continued. About 70% have completed major system upgrades. AI tools have cut compliance and fraud-monitoring costs by 18%. Cybersecurity budgets jumped 27%, a prudent move with cyber threats rising amid global conflict.

March 18: Fed Chooses Patience

The Federal Reserve held rates steady in March (11–1 vote) while noting that U.S. credit conditions remain “stable.” Markets now expect the first rate cut in September rather than summer. Treasury yields stayed firm near 4.4% on the 2-year note.

Market Fallout and the Real Economy

March’s chaos filtered quickly into daily life. Oil spiked to almost $120 before falling below $88 after coordinated reserve releases. Gasoline remains about 11% more expensive than in February. Consumers cut back: discretionary card spending fell 2.1% month-to-month.

Energy swings boosted commodity-trading income enough to offset other slowdowns. For now, the consumer economy is cooling but not cracking.

Credit Pressure, Not Crisis

Underneath the headlines, short-term corporate funding shows some hesitation. March saw a 9% drop in commercial-paper issuance, the sharpest since 2023. Leveraged-loan spreads widened, then retraced. Credit default swap prices tightened again by month-end, implying that fear may already be priced in.

Tech Turbulence Spreads to Finance

The Nasdaq’s 7% slide since mid-February trimmed portfolios across desks. Global trading units made up ground as bond and FX volatility fueled profits. Smaller lenders with venture loan exposure face tougher quarters ahead as startup valuations wobble.

Washington and Policy Shifts

Congressional debates grew louder on “shadow credit”, the lightly regulated world of private funds and direct lending. The Treasury has launched a transparency review, with draft guidance likely by summer. The White House encouraged domestic oil output to tame fuel prices, complicating “green finance” initiatives.

Investor Rotation and Refuge

ETF flows show that investors are getting defensive again. Dividend oriented funds rose 6.4% in March, while momentum funds bled assets. A Schwab survey found 57% of clients confident in U.S. financials, the highest reading in four years.

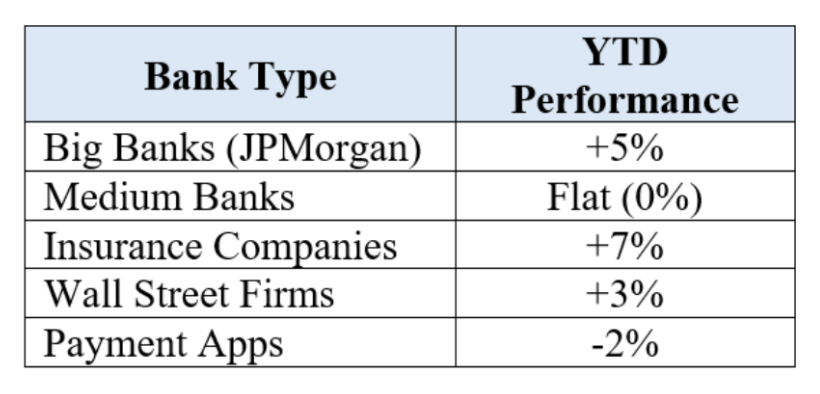

Insurance Quietly Leads

While other areas drew focus, the insurance industry outperformed all major financial subsectors, up 7% year-to-date. The reason: pricing power. Higher shipping, trade, and cyber-risk premiums are offsetting modest investment returns. Cyber insurance, up 40% in policy demand, has become a growth engine for AIG, Chubb, and Travelers.

Global Contrast

U.S. financials continue to outshine peers abroad. European lenders report under 1% loan growth; Asian institutions wrestle with disinflation. Japan’s March rate hike drew global capital back to U.S. debt, strengthening the dollar around ¥142.

Employment and Efficiency

Financial-sector layoffs, roughly 6,000 in March, came mostly from fintech and advisory units. Wage growth eased to 3.4%, reducing cost pressure. AI tools have pushed expense ratios down 15–20% year-on-year.

What to Watch Next

- Rates and Inflation: Energy linked inflation could delay rate cuts beyond summer.

- Private Fund Liquidity: Congressional reviews in April will test transparency promises.

- Office Loans: Vacancy rising to 23% poses refinancing challenges mid-year.

- Corporate Credit Revival: If energy prices settle, loan demand should rebound by Q2.

- Geopolitical Wildcards: A cease-fire pushing oil below $85 would instantly lift sentiment.

Bottom Line

Three months into 2026, the U.S. finance sector has taken a direct hit from war headlines, oil volatility, and market corrections, and stayed upright. The system’s heavyweights are not sprinting ahead, but their endurance alone speaks volumes. Huge capital cushions, nimble technology, and investors rediscovering value have given banks room to breathe.

In times of turbulence, survival itself becomes strategy. The past month showed that U.S. financial institutions can absorb shock and adapt quickly, a skill set increasingly worth more than speed or risk-taking. The next chapters will test whether “steady” can remain profitable. For now, that steadiness is victory enough.