Argo Gold Inc.

Triple Play Opportunity: Gold, Oil, and Uranium – Initiating Coverage

Published: Feb 28, 2026

Author: FRC Analysts

Disclosure: Argo Gold Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions.

Company Details

Sector – Basic Materials

Industry – Gold

Trading Information

Trading information – ARQ.CN : CSE

Report Highlights

- Argo is focused on high-grade exploration-stage gold projects in Ontario and Saskatchewan, oil production in Alberta, and uranium claims in the Athabasca Basin. A key differentiator is that Argo offers rare exposure to gold, oil, and uranium, a combination uncommon among junior resource companies. All three commodities are in focus at the moment: gold is near all-time highs despite a recent pullback, oil is in focus due to geopolitical events, and uranium is increasingly being looked at to power AI data centers.

- Renowned mining investor Eric Sprott owns 16% of the company’s equity, reflecting confidence in the management team, and the quality of its portfolio.

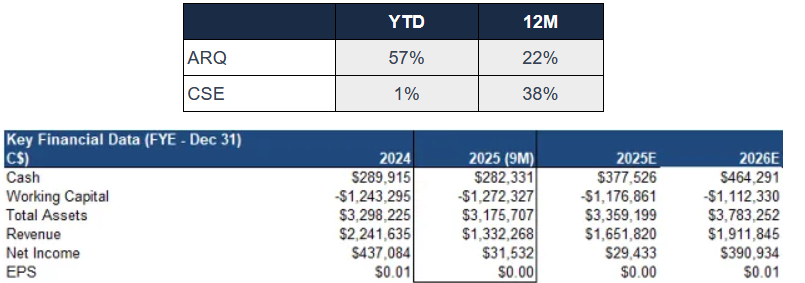

- The company has been profitable since 2024, driven by oil production. All exploration and G&A costs have been fully funded by oil revenue, resulting in no share dilution.

- Argo generates roughly $1M in operating profit per year from oil production, supported by an independent valuation of its oil assets at $15M. For context, Argo’s current MCAP is just $8M, meaning the market is not only undervaluing the oil assets, but also completely discounting the gold and uranium projects.

- Argo also controls several early-stage gold, silver, and uranium projects, most of which are near well-known projects held by larger companies. Proximity to major players is important, as a successful discovery could make a project an attractive acquisition target.

- Management has outlined an exploration target of 0.45 Moz of gold at exceptionally high grades (not independently verified or NI 43-101 compliant) across two projects. While modest in size, we believe the unusually high grades make the projects attractive. We estimate the value of these resources alone at $0.20/share.

- Gold has retreated from historic highs but remains up 73% YoY, sustaining unprecedented levels. While short-term volatility can be severe, we expect prices to stay well above historical averages, supported by safe-haven demand amid geopolitical uncertainty.

- Upcoming catalysts include potential new wells in Alberta, exploration at its gold, silver, and uranium projects, and increased market recognition of the intrinsic value of its portfolio.

Risks

- The value of the company is dependent on commodity prices

- Gold and uranium projects lack a NI 43-101 compliant resource

- Exploration and development

- There is no assurance that the company can advance its projects simultaneously

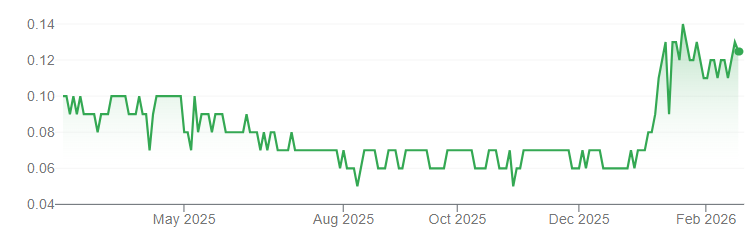

Price and Volume (1-year)

* Qualified Person: Michael Guo, PhD, PGeo, MG Geological Consulting Ltd

* Argo Gold Inc. has paid FRC a fee for research coverage and distribution of reports. See last page for other important disclosures, rating, and risk definitions. All figures in C$ unless otherwise specified.

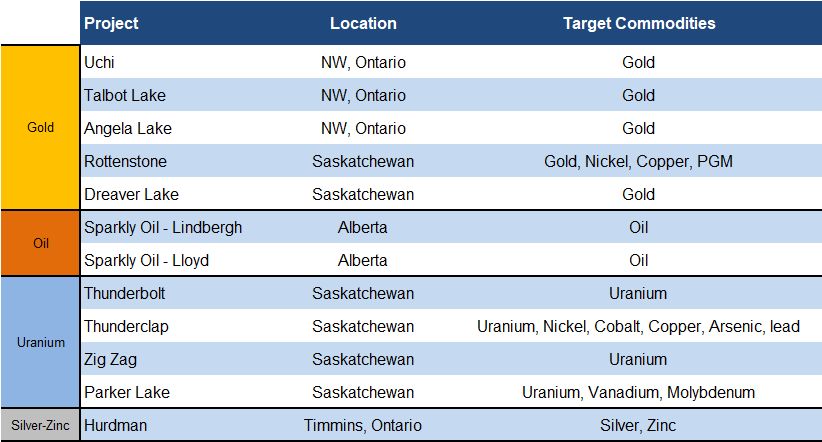

Five gold projects and a silver-zinc project in Ontario and Saskatchewan, oil production in Alberta, and four uranium projects in Saskatchewan

Portfolio Summary

Source: Company / FRC

The following sections summarize ARQ’s flagship projects.

Sparky Oil Project

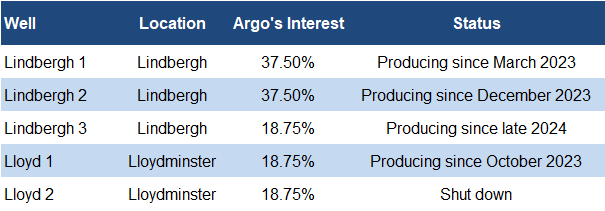

During 2023–2024, Argo invested $2.6M to develop five oil wells in Alberta, operated by Croverro Energy , a private oil producer in Alberta and Saskatchewan. Four wells are currently producing.

ARQ made its first oil investment in 2023

Project Location

Source: Company

Wells are located in Lloydminster and Lindbergh, producing heavy oil

Heavy oil is denser, more viscous, and lower in API gravity (<22 API), making it harder to refine and generally selling at a discount to light oil, which flows easily and yields more high-value products. Heavy oil wells typically have modest initial production , but can maintain output steadily for 7–10 years, whereas light oil wells often start higher but decline faster.

Oil Type & Production Profile

A standard well in Argo’s target regions, often horizontal or multilateral to maximize reservoir contact, produces roughly 80–120 bpd, with a moderate decline rate of 10–15% per year in the early years. Drilling costs are typically $1–2 M per well, with OPEX around $15/bbl, making them relatively low-CAPEX and low-OPEX projects. This efficiency is because the wells target the Sparky Formation , a shallow layer at 450–650 m, which keeps drilling costs low, combined with high pressure and good permeability, allowing production without expensive injection methods.

Well Design & Economics

Argo’s Wells

The opinions expressed in this report are the true opinions of the analyst(s) about any companies and industries mentioned. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The companies listed above are covered by FRC under an issuer-paid model, where fees have been paid to FRC to commission this report and research coverage. This creates a potential conflict of interest which readers should consider. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. To subscribe for real-time access to research, visit https://www.researchfrc.com/plans for subscription options. This report contains “forward looking” statements. Forward-looking statements regarding the Company, industry, and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company’s products/services in the marketplace; acceptance in the marketplace of the Company’s new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company’s periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward-looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.